In accounting, the claims of creditors are referred to as liabilities and the claims of owner are referred to as owner’s equity. When the total assets of a business increase, then its total liabilities or owner’s equity also increase. Accountants and members of a company’s financial team are the primary users of the accounting equation. Understanding how to use the formula is a crucial skill for accountants because it’s a quick way to check the accuracy of transaction records . These may include loans, accounts payable, mortgages, deferred revenues, bond issues, warranties, and accrued expenses.

Fact Checked

One of the main financial statements (along with the balance sheet, the statement of cash flows, and the statement of stockholders’ equity). The income statement is also referred to as the profit and loss statement, P&L, statement of income, and the statement of operations. The income statement reports the revenues, gains, expenses, losses, net income and other totals for the period of time shown in the heading of the statement. If a company’s stock is publicly traded, earnings per share must appear on the face of the income statement.

Submit to get your question answered.

The combined balance of liabilities and capital is also at $50,000. To make the Accounting Equation topic even easier to understand, we created a collection of premium materials called AccountingCoach PRO. Our PRO users get lifetime access to our accounting equation visual tutorial, cheat sheet, flashcards, quick test, and more. The accounting equation is fundamental to the double-entry bookkeeping practice. Its applications in accountancy and economics are thus diverse. This is how the accounting equation of Laura’s business looks like after incorporating the effects of all transactions at the end of month 1.

- Before explaining what this means and why the accounting equation should always balance, let’s review the meaning of the terms assets, liabilities, and owners’ equity.

- Some assets are tangible like cash while others are theoretical or intangible like goodwill or copyrights.

- This simple, easy-to-understand tool can tell you what you need to know upfront so you know what to focus on if there are any issues or room for improvement.

- In fact, most businesses don’t rely on single-entry accounting because they need more than what single-entry can provide.

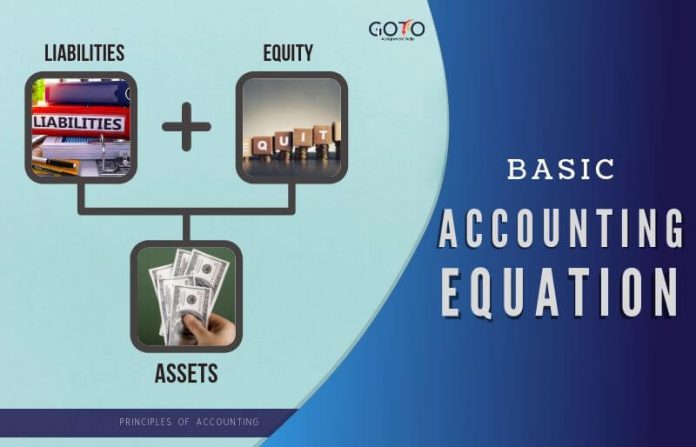

- The accounting equation shows the amount of resources available to a business on the left side (Assets) and those who have a claim on those resources on the right side (Liabilities + Equity).

- In the above transaction, Assets increased as a result of the increase in Cash.

Let’s add transaction #3:

This formula represents the accounting identity, which must always be true for all entities regardless of their business activity. Owners equity, or simply, equity, loans and grants is the value of the business assets that the owner can lay claim to. The amount of liabilities represents the value of the business assets that are owed to others.

What Is Shareholders’ Equity in the Accounting Equation?

He forms Speakers, Inc. and contributes $100,000 to the company in exchange for all of its newly issued shares. This business transaction increases company cash and increases equity by the same amount. While the accounting equation goes hand-in-hand with the balance sheet, it is also a fundamental aspect of the double-entry accounting system.

Do you already work with a financial advisor?

To learn more about the balance sheet, see our Balance Sheet Outline. For the past 52 years, Harold Averkamp (CPA, MBA) has worked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online. Metro Corporation earned a total of $10,000 in service revenue from clients who will pay in 30 days. Shaun Conrad is a Certified Public Accountant and CPA exam expert with a passion for teaching. After almost a decade of experience in public accounting, he created MyAccountingCourse.com to help people learn accounting & finance, pass the CPA exam, and start their career.

The remainder is the shareholders’ equity, which would be returned to them. In other words, the total amount of all assets will always equal the sum of liabilities and shareholders’ equity. The double-entry practice ensures that the accounting equation always remains balanced, meaning that the left-side value of the equation will always match the right-side value.

So, as long as you account for everything correctly, the accounting equation will always balance no matter how many transactions are involved. The accounting equation’s left side represents everything a business has (assets), and the right side shows what a business owes to creditors and owners (liabilities and equity). As you can see, all of these transactions always balance out the accounting equation. This straightforward relationship between assets, liabilities, and equity is the foundation of the double-entry accounting system. That is, each entry made on the Debit side has a corresponding entry on the Credit side.

If the net amount is a negative amount, it is referred to as a net loss. The assets have been decreased by $696 but liabilities have decreased by $969 which must have caused the accounting equation to go out of balance. To calculate the accounting equation, we first need to work out the amounts of each asset, liability, and equity in Laura’s business. Like any brand new business, it has no assets, liabilities, or equity at the start, which means that its accounting equation will have zero on both sides. This arrangement is used to highlight the creditors instead of the owners. So, if a creditor or lender wants to highlight the owner’s equity, this version helps paint a clearer picture if all assets are sold, and the funds are used to settle debts first.